There are a number of key tax considerations to take into account when putting together a business structure to maximise tax efficiency and minimise risk, including:

- Tax effective asset protection

- Tax efficiency and flexibility

- Exit options

Asset protection

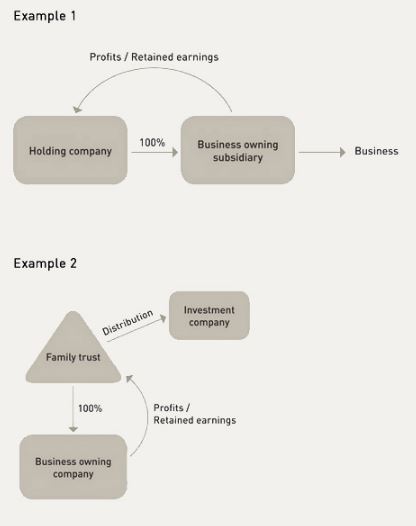

We often see business structures whereby retained earnings are kept in the same entity that operates the business. If a customer or an employee of the business was to sue that entity, the retained earnings sitting within that entity would be at risk. A far better structure is one that enables the retained earnings to be passed out of the main trading entity to another entity in a tax effective way.

Here are some examples that illustrate this concept:

In each of these cases, tax will have been paid on profits generated by the business owning company at a rate of 30 percent. These profits can be distributed out of that entity by way of dividend, meaning that they will no longer be available to satisfy claims of creditors of the business owning company.

The dividends will carry franking credits for the tax already paid. In both of the examples above, these dividends flow through to another company, and so no additional tax is payable.

Tax efficiency and flexibility

Losses are often generated in the start-up phase of a business. Some structures allow these losses to be utilised by flowing them through to another entity to offset income of that other entity, while others do not.

For example, a company cannot pass losses through it - they must be carried forward until the company generates taxable income to offset the losses. Contrast this with a partnership, where both income and losses flow through the partnership to the partners. An example of the best of both worlds is a partnership which consists of a number of trusts, each trust representing an individual partner. Losses incurred by the partnership flow through to the trusts and can be utilised to offset other income in those trusts.

Family trusts or discretionary trusts generally also provide tax efficient outcomes. If nothing more, they are extremely flexible in allowing you to determine which beneficiaries will be taxed on the trust income. Furthermore, distributions can be made to company beneficiaries in order to effectively cap the tax to 30 percent. Further tax efficiencies can also be obtained by using as many low marginal tax rate beneficiaries as possible (eg children over 18 years of age).

In contrast, companies do not provide as much flexibility as trusts in terms of tax efficiency.

Exit options

It is important for business owners to constantly reassess their exit strategy and the tax consequences that will flow from it.

What happens if a business owner wants to allow external investors to invest in the business? Does the structure allow for this in a tax efficient manner?

What happens if the business owner wants his or her son or daughter to become involved in the business, or to take over the business after the owner's death? Is tax payable when the business is transferred to the next generation?

Often, there is a balancing exercise between these outcomes. For example, a family trust does not readily allow for external investors to come into the business, but is an excellent vehicle for allowing the business to be passed on to the next generation in a tax efficient way.

However, a family trust is not a suitable vehicle for an IPO. If an IPO is intended, assets would need to be transferred out of the family trust into a company structure, potentially triggering CGT and stamp duty consequences.

Companies can allow external investors to come in as shareholders, whether on a small scale or by way of IPO.

Further, if a trade sale is intended, then that sale may proceed by way of either an asset sale or a share sale. We are seeing more of an appetite for share sales given the potential stamp duty savings and the fact that sellers can utilise the 50 percent general CGT discount. Purchasers may also be able to subsume the newly acquired company into their tax consolidated group. In this situation, a purchaser may wish to limit its potential exposure to any previous indiscretions of the newly acquired company by transferring the assets out of that company to another member of the tax consolidated group, thereby avoiding CGT and potentially stamp duty. The newly acquired entity can then be wound up.

Summary

The structure adopted by business owners will often be a compromise between the immediate requirements of the business as initially set up, those requirements in the midlife of the business (together with competing asset protection, flexibility and tax efficiency outcomes), and the ultimate exit option to be pursued by the business owner. It is rare to find one structure that can fulfil all these roles at all times in a tax effective way. Analysis of your business structure should be undertaken on a regular basis, and, at a minimum, whenever the business undergoes a significant event.

For more information on structuring your business for tax efficiency, please contact HopgoodGanim's Taxation and Revenue team.